Overview of AZ Charitable Tax Credit

The information below is compiled from the AZ Dept of Revenue’s Form 321i and Form 352i instructions. Always speak with your tax expert regarding any tax matters.

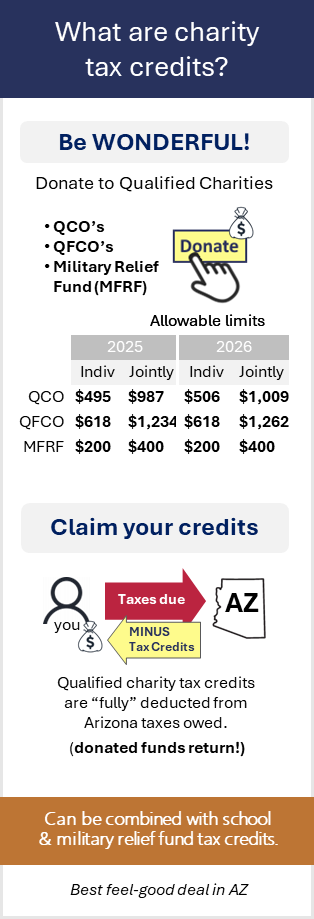

- A tax credit, unlike a tax deduction, is subtracted in full from Arizona income taxes owed. You get credit for the full amount of your donation up to allowable annual limits.

- A free to redistribute, downloadable 2026 PDF detailing QCO, QFCO, MFRF and school tax credits, limits, deadlines, carryover rules. AZDOR forms and qualified organization links.

- To receive a charitable tax credit, financial donations MUST be to a qualified charity (QCOs) and/or qualified foster care (QFCOs). Military Family Relief Fund (MFRF) donation must be made before the annual $1M limit is reached.

- Charitable Tax Credits are fully deducted from AZ income taxes owed using Form 321 (QCOs) and Form 352 (QFCOs). Use Form 340 for Military Relief Fund donations.

- There are annual maximum allowable tax credits for contributions to QCOs and QFCOs. Same for MFRF donations. There is no minimum.

- Charitable, Foster Care, Military Relief Fund and School Tax Credits can ALL BE COMBINED to reduce AZ income taxes due.

- Claimed qualified charity donations as tax credits on your AZ filing, cannot be itemize on your federal return.

- You can split the QCO maximum allowable credit donations between multiple QCOs. The same applies for splitting QFCOs donations.

- QCO and QFCO donations made between Jan 1 to April 15 can be applied to EITHER the previous or current filing year. Accepted MFRF tax credit donations must be made before Dec 31st of the filing year.

- If your taxes owed are less than the QCO and QFCO Tax Credit donations made, the AZ Dept of Revenue allows for a five-year carryover of any unused allowable donation credit. See example below.

During 2026, Mary, a single person, gave $800 in total to three QCOs. In 2026, Mary is allowed a $506 maximum QCO credit. Mary’s 2026 AZ income tax owed is $250. Mary can apply $250 of her QCO tax credit to her 2026 tax liability. Mary now owes $0 (way to go Mary!) and she can also carryover the unused portion of this credit, $256 [$506-$250] to the 2027 tax year.Mary cannot carryover the portion of her charitable donations that was above the $506 maximum QCO credit, in this case that is $294 ($800-$506). But she can claim $294 in her 2026 federal and AZ filings as a charitable contribution if she is using itemized deductions.

Want to support qualified charities, but you are living paycheck to paycheck? Consider making a small monthly donation to qualified charities directly (or through employer payroll charity programs if offered). Either way, speak with your tax advisor about making a small monthly donation to a qualified QCO and/or QFCO based on your expected AZ income taxes due for the year and if you can use Step 3 on IRS W-4 form "You may add to this the amount of any other [expected tax] credits." to re-balance monthly takehome as appropriate in anticipation of the AZ tax credit benefit.